If you’re facing redundancy, understanding your financial entitlements is crucial. Your redundancy package can significantly impact your pension and future financial security. Our expert advisors help you navigate your options to maximise tax-free benefits and secure your long-term financial well-being.

Your redundancy package typically includes:

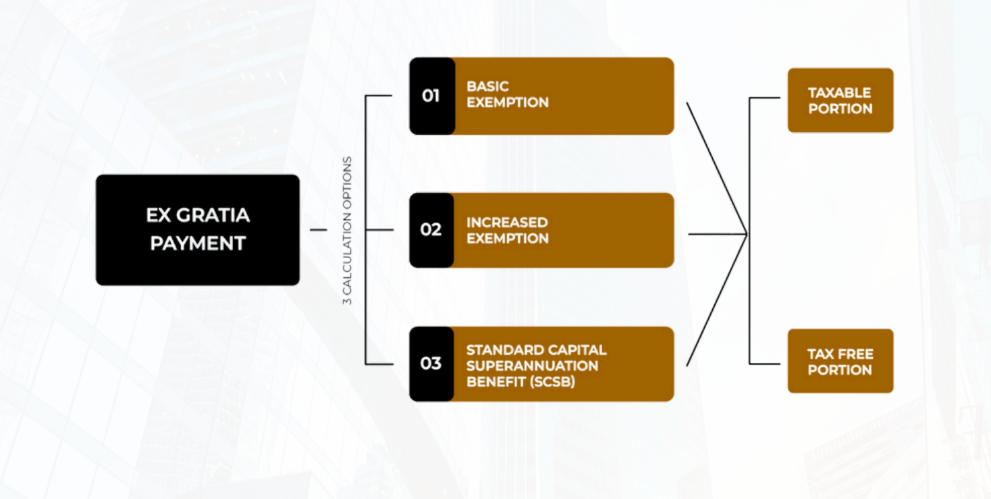

An additional, discretionary payment from your employer as a goodwill gesture.

An additional, discretionary payment from your employer as agoodwill gesture. A portion is tax-free, but the remaining balance is subject to tax atyour marginal rate.

There are three methods to calculate the tax-free portion of your Ex-Gratia payment:Basic Exemption Tax-free amount: €10,160 + €765 for each completed year of service.

Tax-free amount: €10,160 + €765 per completed year of service + €10,000 (minus any previous redundancy or pension tax free lump sums received in past 10 years).

Tax-free amount: (Average earnings over the last 36 months × years of service) ÷ 15 .This method can offer a higher tax-free sum, but you must decide whether to retain or waive your tax-free pension lump sum.

The SCSB calculation differs slightly if you waive or retain your pension lump sum. These calculations are:

To manage cash flow, businesses should also create a budget and regularly review it, comparing actual income and expenses to the budgeted amounts. This can help identify any areas where the business is over or underspending, so that adjustments can be made.

Upon leaving employment, you have several pension transfer options. Each choice impacts your tax benefits and accessibility to funds.

Leave it in your former employer’s scheme Transfer it to a new employer’s scheme (if available) Transfer it to a Personal Retirement Bond (PRB)

Transfer it to a Personal Retirement Savings Account (PRSA) (for tax-free lump sum retention)

If you choose an increased tax-free redundancy payment by waiving your pension lump sum, you can only regain a tax-free lump sum if you transfer your pension into a PRSA. None of the other transfer options allow for a tax-free pension lump sum.

The remaining 75% can be transferred into an Approved Retirement Fund (ARF)

Flexibility to leave funds in the PRSA if immediate access isn’t required

Transferring your pension into a PRSA ensures you retain your tax-free lump sum entitlement (25% of the transfer value).

Early access: From age 50, provided you are fully retired (i.e., no PAYE employment income).

Retiring your PRSA before re-employment ensures: Immediate access to your tax-free lump sum

Choosing the right redundancy and pension transfer option is essential to protect your financial future. Many redundancy package calculations overlook long-term pension implications, leading to costly mistakes. Our expert financial advisors provide personalised guidance to help you:

We’re here to help reach out anytime for expert advice, personalised support, or answers to your financial questions.

We offer Financial Advice to our clients in a very personalised, efficient and friendly service

+353 64 6639164

Mernie joined Money Sense as a Director in 2008 and works in the area of administration and compliance.

Mernie is an Economics and French graduate from UCC.

Mernie also has a postgraduate diploma in Computing and has previously worked in the IT industry for a number of years.

Mernie’s IT experience and business acumen are invaluable in organising and managing the office and maintaining strict compliance requirements.

John is a Qualified Financial Advisor (QFA) who has over 40 years of experience working in the Financial Services Industry.

Having previously worked in the Banking Sector for 28 years, John has acquired significant knowledge and experience in all areas of financial planning and advice.

Establishing Money Sense Financial Services has enabled John to use his extensive experience in providing impartial and sound judgement in the pursuit of better Client solutions in the open marketplace.

John is extremely passionate and committed to his work and prides himself on a positive ‘can do’ attitude. He is very dependable and will do everything in his power to assist customers achieve their financial goals.

In his spare time, John is a staunch GAA enthusiast, being currently involved with Dr. Crokes GAA Club as Manager of their Senior Hurling Team.

Originally from Newtownshandrum, John is a proud Cork man but has settled well in his adopted County and is doing everything in his power to promote the small ball game in Kerry.

John is also a member of Killarney Golf Club with a respectable handicap. John gives 100% in every project he undertakes and exudes positive energy and enthusiasm which can be infectious.